Why I'm Exiting ZETA & Buying This Undervalued Gem

Closing out ZETA as revenue concerns mount, and rotating into a hidden opportunity with stellar earnings growth, high ROIC, and a compelling valuation.

Hey fellow Sharks,

I'm making an adjustment in Portfolio USA today—closing out my position in Zeta (NYSE: ZETA 0.00%↑ ) and rolling the proceeds into a new opportunity that's checking every box on my checklist.

Here's why ZETA is out:

The revenue outlook keeps disappointing—Q1 FY25 guidance missed consensus, and worse, its remaining performance obligations (RPOs), a critical forward-looking indicator, keep sliding. Management keeps talking a big game about growing RFPs by 60%, but after multiple quarters of declining RPOs, I’m skeptical this bullish narrative translates into actual growth.

Profitability growth is decelerating sharply. EBIT margins came in below expectations, weighed down by ramping costs tied to a surge in sales personnel. Zeta might eventually convert these hires into growth, but right now, it's just squeezing margins without clarity on payoff.

Bottom line: The fundamental picture no longer supports staying invested, especially with rising short interest adding volatility. I’m out.

Here's the teaser on what I'm buying:

I’m shifting capital into a name you probably haven't heard much about, yet the financial metrics scream quality and growth:

Trading at a low P/E (~11x) relative to its robust growth trajectory.

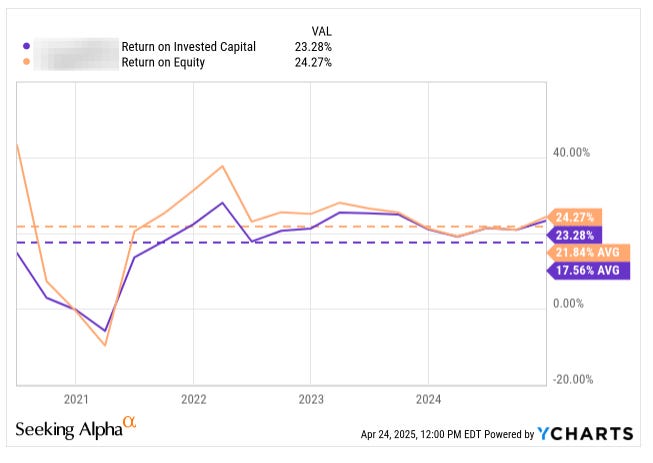

Consistently high ROIC and ROE.

5-year EPS growth (+328%) sharply outpacing revenue growth (+28%).

Benefiting strongly from industry tailwinds, a differentiated business model with AI integration, and exceptional client retention rates, positioning it well to outperform significantly.

Happy investing,

George

Trade details below: