AXIA Deep Dive: A Boring LATAM Utility With a Not-So-Boring +40% Upside

A quiet rebrand made me lose track of this LatAm giant. But the real story is a rare setup: massive uncontracted power, rising demand, and a valuation that still doesn’t reflect the upside.

Update:

Jun8’26: Closed position at $9.71 (-0.6% loss) due to ADRs being delisted.

Apr20’26: Revised target price ($13.40 → $17.45)

On January 8, I sent a trade alert to paid subscribers adding a Latam utility to the portfolio.

A utility should not be this interesting. But this company sits on a rare edge: it has a big chunk of uncontracted electricity capacity. In plain English, it is not locked into decades of “cheap” long-term contracts like most utilities. It can sell more power at today’s higher market prices.

And even better, this “free” capacity is growing over time, which creates a built-in earnings tailwind.

My base case shows +40% upside from here… and yes, we’re talking about a utility.

As most of you know, I came down to Chile to ride out the Canadian winter. And by pure coincidence, a good friend of mine (let’s call him AP) who recently moved back to the US was here at the same time.

So we did what any group of ex-colleagues would do. We grabbed a table and ordered drinks. Later in the evening, AP turned to me and said, “Have you looked at Axia Energia?” The name didn’t ring a bell at first. AP was talking about the old Eletrobras, Brazil’s huge power company I used to cover its bonds back when I worked at Moneda.

I practically spat out my drink. How did I miss that one?

It turns out Axia Energia is Eletrobras, just rebranded and with a new ticker. It had quietly fallen off my stock watchlist because of a ticker change mix-up, and I hadn’t noticed.

Embarrassing? A little.

But mostly, I was excited. Here was a familiar giant in the Brazilian energy world that I’d accidentally ignored, now popping back into view thanks to a friend’s tip. And as I dug deeper, I realized Axia was a far more interesting beast today than the stodgy utility I remembered.

Back then it traded as EBR (for Eletrobras) in New York and as ELET3 in Sao Paulo. But after privatization, they rebranded to Axia Energia and even changed the ticker to AXIA3 in Sao Paulo and AXIA on NYSE. Somewhere in that shuffle, my systems lost track of it.

As I caught up on Electrobras Axia, I noticed big changes from the government sell-down and the new voting cap just to name two. Could it be that this old giant, now wearing new clothes as Axia, was an overlooked opportunity? AP certainly seemed to think so, and I trust his nose for these things.

The following week when I had some time, I refreshed my old model, read the lates 10Ks and everything I could find on Axia Energia. What I discovered was eye-opening. This wasn’t the sleepy, state-run utility I remembered. Axia Energia is now a leaner, more market-driven powerhouse and it has a secret sauce none of its competitors have.

In the Brazilian electricity market, nearly every big generator has sold most of their energy on long-term contracts. But Axia? Thanks to its unique history, it’s the only major player sitting on a mountain of uncontracted capacity that it can sell at juicy market prices as demand spikes.

And demand is spiking (think of all those new cloud computing data centers popping up, which need massive electricity).

Brazil is seeing an electricity boom from things like new data centers and tech infrastructure needing tons of power. Axia is positioned like a vendor at the only water tap in a desert.

Axia’s stock looks undervalued given its flexibility and growth potential, and I estimate a fair value around $13.40. The company can grow earnings by selling its uncontracted power at premium prices, and I expect the market to re-rate Axia’s valuation higher once those fatter margins start rolling in.

Table of Contents:

Company History & Evolution: From Eletrobras Dinosaur to Axia Dynamo

How Axia Makes Money: Unlocking the Power of Free Market Electricity

Management & Capital Allocation: From Fat Dividends to Smart Reinvestments

Company History & Evolution: From Eletrobras Dinosaur to Axia Dynamo

To understand Axia, you have to know where it came from. Axia was known for decades as Eletrobras, the Brazilian government’s electric power juggernaut. Founded in the 1960s, Eletrobras was a behemoth that dominated generation and transmission at one point providing around 30–35% of Brazil’s electricity capacity.

It owned dozens of hydroelectric dams (including Itaipu, one of the world’s largest, jointly operated with Paraguay), wind farms, and even nuclear plants. It also ran nearly half of Brazil’s high-voltage transmission lines. For years, Eletrobras was synonymous with Brazil’s electricity sector; huge, important, but also known for bureaucracy and government meddling.

All that started to change in mid-2022, when Eletrobras was privatized in a landmark share offering. The government, under then-president Bolsonaro, sold down its stake, turning Eletrobras into a corporation with a dispersed shareholder base. The Brazilian state went from owning roughly 60% to holding less than 45% after the offering. Crucially, a new rule capped any shareholder (including the government) at 10% of voting power, even if they owned more stock.

This was meant to prevent any single entity from controlling Axia and to ensure it operates like a private business with professional management. The government did keep a “golden share” which is a special class of share that gives it veto power over certain critical decisions (like possibly blocking foreign control or protecting nuclear assets). But day-to-day, Axia is now run for profit, not politics.

For a while after privatization, there was political noise. Brazil elected a new president (Lula) who was openly unhappy with how Eletrobras was privatized. There were court battles about the government’s role and the 10% voting cap. Investors fretted that the government might try to reassert control.

However, by late 2025 this overhang largely cleared up as a Supreme Court-backed agreement confirmed the 10% voting limit stays, and in exchange the government gets to appoint some board members (3 out of 10) as long as it holds a significant chunk of shares. In other words, the company stays privatized and independent, with the government as an important shareholder but not calling all the shots.

As part of turning the page, Eletrobras rebranded to Axia Energia in October 2025. The name “Axia” (which implies value or axis) was chosen to shed the old image. It even dropped “Brasil” from the name to emphasize the break from state ownership. The ticker symbol on Brazil’s stock exchange changed from ELET3 to AXIA3, and similarly in New York the ADR now trades under AXIA.

Axia became a very different company after the 2022 privatization. The Brazilian government stopped being the controlling shareholder, and Axia now has no controlling shareholder. Even more important, Axia’s bylaws cap voting power at 10% per shareholder or group, regardless of economic ownership, which prevents any single investor from taking control through voting.

SEC Form 6-K excerpt showing 10% voting cap governance structure after Eletrobras privatization, key point in AXIA investment thesis and Brazil utility stock analysis")

Today, the shareholder base is still substantial and institutional. Axia’s own investor relations disclosures show the “Government group” holds about 45% of common shares, but that stake does not translate into control because of the voting cap.

The result is unusual for a Latin American utility of this size. Axia is effectively widely held, and management now has room to run the company with a sharper focus on profitability and capital allocation.

And boy, have they been busy shaking things up. Axia’s management launched an aggressive efficiency drive post-privatization. Freed from government red tape, the company cut costs deeply. In fact, since late 2022 it slashed operating expenses by 18% and reduced headcount by 17%. Consider that Eletrobras had been notorious for bloated payrolls and political appointments; those cuts were a breath of fresh air.

The result?

Profitability jumped. Axia went through a trough in 2023, but profitability inflected meaningfully after privatization. Net income rebounded in 2024 and continued improving into 2025, alongside a clear expansion in EBITDA margins.

They even sold off non-core assets. For example, Axia got rid of its stake in a nuclear power subsidiary in 2025 to focus on its core hydro and transmission business. The new CEO, Ivan de Souza Monteiro, has focused on running Axia “like a business” rather than a bureaucracy. Historically, Eletrobras accumulated odd assets such as a cinema and a hospital, remnants of a time when it effectively built entire towns around large hydro projects. The new Axia is unwinding those legacies and focusing strictly on energy.

Today, Axia is a streamlined version of its former self. It operates 81 power plants across Brazil: 47 hydroelectric dams, 33 wind farms, and 1 large solar farm. All together, Axia accounts for roughly 17% of Brazil’s total power generation capacity (making it the country’s largest single energy supplier).

On the transmission side, it still runs about 37% of Brazil’s electric grid lines. Crucially, over 96% of Axia’s generation comes from clean, low-carbon sources (mainly hydro, plus wind and some nuclear it used to own). This clean profile gives Axia a bit of ESG shine (the company often touts that 100% of its capacity is low-emission).

How Axia Makes Money: Unlocking the Power of Free Market Electricity

Axia’s business is basically to generate electricity and sell it, and to transmit electricity across Brazil’s grid. Sounds simple, but the way this works in Brazil is a bit unique. Brazil has a two-tiered power market: a regulated market and a free market.

In the regulated market, utilities sign long-term contracts (often 15-30 years) through government-organized auctions to supply electricity to distribution companies at fixed prices. In the free market, big consumers (like factories, shopping malls, and lately data centers) or power traders negotiate directly with generators for energy, or generators can sell into the spot market.

Historically, most of Brazil’s electricity has been sold via long-term regulated contracts as it gives stability, but it means prices are often locked in and can be low. Generators with only contracted capacity don’t benefit when market prices rise as they’ve already sold their output cheaply.

Here’s where Axia stands out. Axia has an unusually large share of its capacity that is not locked into long-term contracts. Because of something called the “quota regime” and its end. Back around 2013, many of Eletrobras’s big old hydro plants were put under a quota system: they had to sell power at cost (peanuts, basically) to the regulated market, in exchange for extending their concessions.

These plants only earned a small fixed fee for operation & maintenance (O&M), not real market prices for power. It was a government scheme to keep electricity cheap. Private companies mostly avoided this, but being state-run, Eletrobras went along for many plants.

Fast forward to privatization, and this is where the real change happens. The quota regime is being phased out, turning Axia’s hydro plants into normal power plants that can sell electricity at market prices. By 2027, quota exposure drops to zero. At that point, depending on how aggressively Axia contracts its output, between 29% and 43% of its energy remains uncontracted, based on management’s own hedge assumptions. That is thousands of megawatts exposed to market pricing.

3Q25 energy balance table showing rising uncontracted capacity through 2027, supporting the AXIA stock deep dive and investment thesis on free-market power pricing upside.")

What this means is that Axia can now sell that energy in the free market or in new contracts, likely at much higher prices than the old quota rates. And indeed, we’re already seeing the impact.

In Q3 2025, only about 36% of Axia’s energy volume was sold under the regulated market and legacy quota regime, with the remaining roughly two-thirds already exposed to free and spot market pricing.

deep dive investment thesis table from 3Q25 showing generation revenue breakdown by regulated market and free market, including volume (aMW), average price (R$/MWh), and regulatory revenue performance.")

The spot price (short-term market price) in Brazil jumped in 2025 due to higher demand and other factors, and Axia was able to cash in. Its revenue from the short-term market in Q3 was R$1.76 billion, up 152% from the year before.

In fact, Axia reported that the contribution margin (profit per unit) of its energy sold in the free market/spot nearly doubled from R$48/MWh in Q3 2024 to R$86/MWh in Q3 2025.

That’s because it was no longer forced to sell as much at the old cheap rates. The remaining quotas are dwindling fast (and even the small O&M fees Axia earns from them dropped by 35% as quotas phased out), but the trade-off is way more power to sell freely.

It has far more uncontracted capacity than any other major Brazilian utility. Competitors like Engie Brasil or CPFL often have 90-100% of their capacity tied up in contracts or their own distribution businesses. Axia, by contrast, might have a sizable portion (tens of percent of its 44 GW capacity) available to sell on the free market as of 2025, and that portion is increasing as quotas end. This strategic flexibility means Axia can play the market to its advantage; selling more when prices are high, signing shorter-term deals with industrial clients, etc., rather than being locked into 30-year fixed-price deals.

It’s worth noting Axia has a second business segment: transmission. Operating transmission lines is more of a steady, regulated business. You get paid a fixed fee (adjusted for inflation) for making the lines available, kind of like a toll road for electrons. Axia’s +66,000 km of lines provide stable revenue that isn’t very sensitive to market power prices.

In Q3 2025, for instance, the transmission segment contributed solidly to Axia’s EBITDA with regulated returns. This stability balances the generation side, which can be more volatile. But generation is where the big upside is now, because of that free market exposure.

Let’s sanity-check the trend with the income statement. In the first 9 months of 2025, gross revenue rose 7.0% to R$36.2B, and net revenue rose 9.2% toR$30.8B. Transmission did the heavy lifting as it grew the fastest (10.4%) to R$14.9B. Generation also grew modestly (3.5%).

deep dive investment thesis chart showing 3Q25 vs 3Q24 income statement bridge with gross revenue, net revenue, adjusted EBITDA, and the impact of regulatory remeasurements on transmission contracts under IFRS reporting.")

Yet profitability moved the other way. Adjusted EBITDA fell to R$15.5B (from R$20.8B). The reason sits in one big line item. In 9M24, Axia booked R$6.13B of “regulatory remeasurements” related to transmission contracts. In 9M25, that line flipped to -R$648M. That swing explains a big chunk of the y/y EBITDA drop. The same thing shows up in the quarter. Adjusted EBITDA was R$5.89B in 3Q25, down from R$11.96B in 3Q24, and the “remeasurements” line collapsed from R$6.13B to R$303M.

“Regulatory remeasurements” are accounting gains or losses from revaluing Axia’s regulated transmission contract assets under IFRS. They can swing EBITDA sharply without reflecting real operating performance.

Industry Landscape: A Power-Hungry Brazil

Brazil’s electricity industry is at an inflection point. For the past decade, power demand growth was moderate, and most new supply was snapped up via long-term contracts. But suddenly, a few trends are converging to create surging demand for electricity that isn’t already spoken for. The biggest buzz is around data centers and cloud computing. Brazil is undergoing a data center boom, similar to what we are seeing in the US (read my deep dive on data center in the US here).

Companies like Microsoft [MSFT 0.00%↑] and Amazon (AWS) [AMZN 0.00%↑] are pouring billions into Brazilian data center campuses, and others like Google [GOOG 0.00%↑] and even TikTok’s owner (ByteDance) are following.

These hyperscale data centers consume massive amounts of power. Energy demand from grid-connected data centers in Brazil jumped 330% in one year. And this is just the start: total data center power demand in Brazil could reach 13.2 GW by 2035, up from only 0.7 GW in 2023. That’s nearly a 20-fold increase expected in a dozen years, an almost unheard-of growth curve in a mature power market.

Why do data centers matter here? Because data center operators crave reliable, reasonably priced electricity, and often green electricity (since many have climate goals). They typically strike deals with power producers for dedicated supply. A state like Sergipe in Brazil, which historically had little industry, is now aggressively courting data center projects by highlighting the availability of competitive electricity on the free market.

Axia caught onto this trend: it plans to build a data center adjacent to one of its hydro plants (Xingó in Sergipe) to directly use its power. This strategy of integrating data centers with power generation could give Axia captive high-demand customers.

In general, as data centers proliferate (especially around São Paulo and Rio, where many are clustering), there’s an increased strain on the grid and a need for more power generation. Brazil’s grid is mostly renewable (hydro-heavy), which is great, but that also means in dry years there can be shortages. With new large consumers coming online, every generator with uncontracted capacity is sitting pretty and Axia has the largest uncontracted capacity of all.

It’s not just data centers. Brazil is also pushing EVs (still early, but likely to grow power usage long-term) and even energy-intensive industries like green hydrogen production in the future. One study suggested that by 2060, new uses like EVs, data centers, and hydrogen could quadruple Brazil’s power consumption. I know…I know… that’s far out, but the direction is clear.

In the near term, Brazil’s economy in 2025–2026 is doing relatively well, and electricity consumption typically grows in line with or a bit above GDP. The government’s latest plan shows dozens of new power plants needed to keep up with projected demand growth +4% per year. While Brazil does have significant new renewables being built (solar farms are booming, wind too), most of those are contracted out already. Few companies have spare capacity ready to go like Axia does.

Currently, most of Axia’s peers operate either under the old utility model (long-term contracts, regulated returns) or are much smaller players. For example, Engie Brasil has about 13 GW of capacity (one-third of Axia’s) and generally keeps nearly 100% of it contracted at any given time. CPFL Energia, another big utility, is actually majority-owned by China’s State Grid and focuses on distribution grids and some generation (4 GW) which is also mostly contracted or for its own distributors. Omega Energia is a newer renewable energy company that sells power from wind/solar projects, but it’s much smaller and often signs long-term corporate PPAs (power purchase agreements) to finance its farms.

In other words, no other major Brazilian generator has the flexibility Axia has to sell into a hot market. If a big data center needs, say, 100 MW on short notice, Axia can deliver from its existing plants; competitors might say, “we’d love to, but our output is already committed for the next 10 years.”

This unique positioning is why I describe Axia as an only vendor at the water tap when a crowd of thirsty buyers shows up. In power terms, Axia can negotiate better prices and terms for new contracts than peers who are just fulfilling old contracts. Also by being so large, Axia can influence market prices to some extent by choosing how much to sell on the spot market. During tight supply periods, Axia benefits disproportionately because it has more uncontracted volume that can capture high spot prices.

One more angle: Brazil’s energy mix is highly renewable (which is good) but also weather-dependent (which can cause volatility). Hydro power can vary with rainfall. Axia, with many large hydro reservoirs, can buffer some of this by managing water storage, but climate swings (like El Niño or La Niña years) affect output.

In dry years when power is scarce, prices shoot up and Axia again would win because it can sell its uncontracted portion at scarcity prices. In wet years, prices fall, but Axia’s scale and low costs (hydro is very cheap to operate) mean it can still profit and even choose to contract more if needed.

Competitors & Peers: How Axia Stacks Up

Now, let’s compare Axia to some key peers to see just how different it is. In Brazil, the big generation companies include names like Engie Brasil, CPFL Energia, Cemig, Neoenergia, and Omega Energia.

Regionally, if we look at Latin American power companies trading as ADRs, we might consider Pampa Energia (Argentina), Enel Chile and Edenor (an Argentine electric distribution company).

Engie Brasil

Part of French Engie group, it has 13 GW of mostly contracted power (gas, hydro, solar). Engie runs a tight ship and has stable cash flows, but growth is limited since it must build new plants to expand. Its latest management report confirms that most of its capacity is contracted or allocated, so it doesn’t enjoy upside from spot price spikes.

deep dive investment thesis competitor analysis screenshot showing Engie Brasil Energia stating it keeps most of its energy portfolio contracted long term, highlighting why Axia’s uncontracted capacity offers higher upside.")

Governance-wise, it’s controlled by Engie (France) with 68% ownership, meaning minorities follow the controlling shareholder’s strategy. Engie’s valuation tends to be moderate and investors see it as a bond-like steady utility.

CPFL Energia

Based in São Paulo, CPFL has a big power distribution business and about 4 GW of generation. It’s majority-owned (over 50%) by China’s State Grid. That means it’s essentially under a foreign state-controlled parent, and its float is smaller.

CPFL’s generation is largely through long-term contracts and also via its subsidiary CPFL Renováveis (renewables arm). It doesn’t have the freedom to roam the market like Axia. CPFL’s focus is also split because distribution (wires to customers) is its core, which is fully regulated. CPFL is solid but not particularly dynamic as it’s priced for its steady dividends and Chinese backing.

Omega Energia

It was founded in 2008 and built a renewables-focused platform across wind, hydro, and solar. Over time, it also expanded into energy commercialization, which matters because it pushed Omega toward a more market-oriented mindset instead of just being a passive asset owner.

Omega later combined with AES Brasil, and the business now sits inside Auren Energia (AURE3). The combined platform is no longer “small”, with Auren reporting 8,798 MW of installed capacity as of December 2024.

The bigger takeaway is this: Omega helped prove that “merchant” or free-market renewables can earn strong returns in Brazil, but those models also carry more pricing and hydrology risk than fully contracted utilities.

Cemig (CIG)

A Brazilian utility from Minas Gerais state. Cemig generates power and distributes it in its state. It’s still controlled by the Minas Gerais state government, which owns >50% of voting shares. So it’s somewhat like old Eletrobras: a partially state-run firm. Cemig has about 6 GW capacity but much is contracted or used for its own customers.

Pampa Energia (PAM)

An Argentine company (so a very different market). Pampa generates electricity and also has oil/gas assets. Argentina’s market is heavily regulated and currently troubled, so Pampa’s multiples are weird (it might trade at 4.4x EBITDA forward, but Argentine risk is huge (I love playing the Argentinian plays but there is a right moment for that as I did with SUPV (here) and CAAP (here).

deep dive valuation chart showing forward EV/EBITDA comparison versus Latin American utilities including Enel Chile (ENIC), Cemig (CIG), and Pampa Energia (PAM), supporting Axia investment thesis upside.")

Enel Chile (ENIC)

Chilean power generation and distribution company, majority-owned by Italy’s Enel. Chile’s power market is fully private and competitive. Enel Chile trades around 7.6x EV/EBITDA forward.

It has decent growth but is constrained by controlling shareholder and Chile’s moderate market size. Governance is okay, though majority ownership by Enel means strategies align with the parent’s global plans.

By the way, I like this company and have invested in the past in the stock. So we may enter again in the future.

So, how does Axia compare?

First, scale and flexibility: Axia’s 44 GW (gross) capacity dwarfs any Brazilian peer (more than 3x Engie Brasil and 11x CPFL’s generation). That alone gives it advantages in portfolio management. Axia can shift power between regions (it’s present in almost every state) and optimize where it sells. None of the others have that national reach.

Second, contract mix: Axia might have, say, 30–40% of its energy uncontracted, whereas others are 0–10% uncontracted. This is a night-and-day difference in earnings potential when prices rise.

In terms of governance and ownership: Axia, with no controlling shareholder (>10%), is essentially run by professionals under the oversight of a board that includes government appointees and independent directors. It’s not often you see a company of this size with truly dispersed ownership in Latin America. This can be positive (no single shareholder can tunnel resources or impose unfair decisions) and also a challenge (sometimes dispersed ownership companies can lack strategic direction).

However, the Brazilian government1 still having a 45% economic stake means it cares about Axia’s success and has a vested interest in dividends, etc., but it can’t dictate daily operations.

deep dive chart showing December 2025 common share ownership split between government group (45.22%), non-resident shareholders (31.49%), and resident shareholders (23.29%), supporting AXIA investment thesis on governance and privatization.")

Versus peers: Engie and Enel Chile have strong strategic parents but that also means minority investors don’t control fate; CPFL is under Chinese state control; Cemig under Brazilian state control. On balance, I’d say Axia’s governance post-privatization is a big improvement as it has to adhere to higher transparency (SEC in the US as it has ADRs and Brazil’s Level 1 governance segment). The golden share is a minor footnote if the company tries something drastic like moving HQ abroad or selling nuclear plants, which isn’t on the table.

One more peer group helps frame the valuation gap: renewable IPPs and power producers. Clearway Energy trades at 11.2x forward EBITDA, Brookfield Renewable at 13.7x, and NextEra Energy at 14.3x. Even more mixed or merchant-heavy players like AES and Vistra trade in the 11–15x range. At the low end, NRG still trades above 7x.

deep dive valuation chart comparing forward EV/EBITDA multiples vs global utilities and IPPs including Clearway (CWEN), Brookfield Renewable (BEPC), NextEra (NEE), AES (AES), Vistra (VST), and NRG (NRG), highlighting AXIA trading at a discount in this investment thesis.")

Axia, at roughly 7x, sits at the bottom of this group. That valuation still treats it like a legacy utility. But the business is starting to resemble a renewable-heavy IPP, with a growing share of output exposed to market pricing. The difference is that Axia’s growth comes from unlocking existing hydro capacity rather than building new plants. If the market starts to view Axia through that lens, a re-rating toward 10–11x EBITDA would only bring it closer to where comparable U.S. IPPs already trade.

Management & Capital Allocation: From Fat Dividends to Smart Reinvestments

Post-privatization, Axia’s management has two main tasks: improve the business operations (I’ve covered cost-cutting and selling strategy) and decide how to reward shareholders versus reinvesting.

Under government ownership, Eletrobras used to pay decent dividends, but it also had to fund lots of projects (sometimes politically driven) and bailouts (it had to invest in projects like huge hydros Belo Monte, or keep tariffs low, etc.). Now, Axia’s approach is more shareholder-friendly and strategic.

The current CEO and leadership have proven quite capable. After privatization, Wilson Ferreira Jr., who had successfully led Eletrobras before, returned to steer the initial transition. He’s known for improving efficiency (he reduced headcount massively in his first stint). In 2023, Ivan Monteiro (a respected former Petrobras CEO) took over. Monteiro navigated the sticky politics with Brasilia and got that agreement in place to secure governance.

Management’s credibility is seen in their bold moves: they quickly announced asset sales (like the nuclear stake sale), executed a voluntary buyout program for employees, and set clearer performance targets. Morale reportedly improved as the company shook off its old nickname of a bureaucratic dinosaur.

One very interesting piece of Axia’s capital allocation is what it did in December 2025. Axia capitalized R$30.0 billion of profit reserves and issued 606.8 million new Class C preferred shares (PNC) as a stock bonus.

If you owned Axia on the Dec 19, 2025 record date, you received 0.2628378881074 new PNC shares for every 1 common share you held. That’s about a 26% “stock dividend,” paid in a new preferred class. In the U.S., those preferred ADSs trade as AXIA PRC.

This matters for one simple reason: it makes the “drop from highs” in the common stock look worse than it really is.

stock price candlestick chart showing recent volatility and pullback after the rebrand from Eletrobras, used in this AXIA deep dive investment thesis to highlight current entry point and upside potential.")

Axia’s common started trading ex-rights on Dec 22, 2025. “Ex-rights” means new buyers no longer get the bonus shares. The market adjusts for that. FINRA describes the same logic for dividends and distributions: on and after the ex-date, the security trades without the distribution included in the price.

So if you look only at the common chart, you see a sudden step down. But that is not a real destruction of value by itself. The value largely moved from “common only” into “common plus the new preferred you received.” That’s why some holders, like John, saw their total position barely change when they added the preferred to the common.

stock, the AXIA PRC preferred share distribution, and why the post-reorganization price drop may be technical, used as supporting context in this AXIA deep dive investment thesis.")

Now, why do this at all?

Brazil also passed a new tax law that starts in 2026 and adds withholding on dividends in several cases. Companies now have more incentive to think creatively about how they return value. A stock bonus funded by reserves is not a cash dividend, and it can change the timing and character of taxation depending on the investor.

From a capital allocation perspective, Axia has a lot on its plate: it can invest in upgrading old plants, maybe adding solar plants (it mentioned renewable investments in the Amazon and other places), and expanding transmission lines (Brazil auctions new transmission projects regularly, and Axia signaled it wants to participate in those growth opportunities).

In a recent Reuters interview, Axia’s CEO said the company is entering a “new growth phase” including possibly building/buying new power plants and transmission assets. That’s a shift from the past where Eletrobras was often cash-starved and couldn’t invest efficiently. Now Axia can raise capital or use its cash flow to grow where it makes sense, as a private enterprise aiming for ROI.

One more moving piece is debt. Axia has R$72B of gross debt including derivatives and net debt lands at R$42.6B. On that base, net leverage sits at 1.9x LTM adjusted regulatory EBITDA, so the balance sheet looks leveraged, but not stretched.

balance sheet table showing gross debt, cash, net debt of R$42.6B, and leverage of 1.9x adjusted net debt to adjusted regulatory EBITDA LTM as of 09/30/2025, used in this AXIA deep dive investment thesis.")

The maturity ladder also looks manageable. The biggest bucket comes from 2031 to 2035 at R$29.6B.

debt maturity schedule chart showing major maturities concentrated in 2031–2035 (R$29.6B) with smaller amounts from 2025–2030, highlighting refinancing risk and balance sheet outlook in this AXIA deep dive investment thesis.")

The real sensitivity sits in the indexation mix, not the calendar. Roughly 53% of debt is CDI+, another 6% is % of CDI, and 34% is IPCA-linked. A big chunk of Axia’s interest bill moves with Brazilian rates and inflation. If CDI keeps drifting down, Axia wins fast. If inflation spikes, the IPCA-linked portion can sting.

debt maturity schedule chart showing major maturities concentrated in 2031–2035 (R$29.6B) with smaller amounts from 2025–2030, highlighting refinancing risk and balance sheet outlook in this AXIA deep dive investment thesis.")

So management has a three-way tradeoff: pay down debt, invest in growth, and return capital. With leverage around 1.9x and a debt wall that pushes out past 2030, Axia has time. The smart play is to keep refinancing and chip away at the most expensive CDI-linked debt while the company’s post-privatization credit profile keeps improving.

Valuation

At the time of writing, Axia trades around $9.50 per ADR. One ADR equals one common share. I obtain a fair value of $13.40 using a DCF model. The main assumptions are below:

DCF valuation assumptions table showing forecast revenue growth, EBIT margin expansion, tax rate, and capex intensity from 2025 to 2036, used in this AXIA stock deep dive investment thesis and fair value model.")

Revenue

The key growth mechanic is the quota regime phase-out. That regime forced Axia to sell a large share of hydro output at regulated prices and low economics. And that share drops like clockwork . From Axia’s SEC filing, the “old quotas” exposure steps down 20% per year until it hits zero in 2027 (100% in 2022, then 80%, 60%, 40%, 20%, and 0%).

So this is not a “maybe.” It is a scheduled and large unlock. Fitch estimates Axia’s available energy for allocation rises from 3.0 GW in 2025 to 7.6 GW by 2027, as decotization frees up more supply.

And the pricing gap matters. As quotas roll off, Axia’s “uncontracted” energy position expands hard, going from 15% in 2025 to 32% in 2026, and 43% in 2027.

Even more important, my base-case pricing assumptions already imply a very different earnings profile versus the legacy world. My average realized energy sales prices around BRL 180/MWh (2025), BRL 190/MWh (2026), and BRL 200/MWh (2027), while calling out older legacy contracts around BRL 90/MWh.

Hydro has low marginal costs. So when price per MWh rises, the incremental revenue falls disproportionately to EBITDA.

The transmission side of Axia looks like a regulated infrastructure annuity. The revenue comes from RAP-style contracts, and those contracts typically carry inflation-linked annual adjustments (indexation can differ depending on the concession, but the point stays the same: it updates with inflation, not market mood).

So I keep transmission growth more conservative and treat it as the “base load” of the model. It won’t triple. It also won’t disappear.

That’s also why I fade into a 4.4% long-term growth rate from 2031 onward. That assumption matches a utility reality. You get inflation plus modest real expansion.

EBIT

I model Axia’s EBIT margin stepping up into the high 41%s as the quota phase-out finishes and market pricing becomes the dominant driver.

Free-market contracting prices around R$252/MWh in 2026…

Brazil power market system data table showing GSF hydrology level and PLD spot electricity prices (R$/MWh) by region in 3Q25 vs 3Q24, supporting this AXIA stock deep dive and investment thesis.")

… while the energy leaving quotas sits closer to R$94/MWh.

generation revenue table by contracting environment (regulated market vs free market) showing volume, average price (R$/MWh) and revenue in 3Q25, highlighting quota energy priced near R$94/MWh versus higher market pricing in this AXIA deep dive investment thesis.")

The reason is simple. Hydro has low marginal costs. So when the selling price per MWh rises, most of that uplift turns into profit.

And you can already see the mechanics in Axia’s own disclosures. In 3Q25, they pointed out that available resources increased as more volume got released by the gradual phasing out of legacy contracts (decotization), even though hydrology worsened and GSF fell. And you can already see this effect in reported unit economics:

In 3Q25, Axia’s contribution margin for bilateral contracts + spot exposure (ACL + MCP) rose to R$86/MWh from R$48/MWh a year earlier.

In the same update, Axia pointed out unit margins rose from R$55/MWh to R$95/MWh y/y.

That’s the key. The “free” volume expands structurally over time. Axia can route more MWh through ACL and spot, instead of quota economics.

Capex

I model capex at 8% of revenue and gradually decreasing to 6%. The mix matters though. I don’t assume some giant hydro buildout. I assume transmission absorbs the bulk of growth capex, while generation stays more maintenance-heavy.

The company’s own numbers support that transmission bias. In 3Q25 alone, Axia reported R$2.7B of investments.

3Q25 investment breakdown showing R$2.701B total capex allocation with R$1.203B to transmission and R$677M to Itaipu HVDC modernization, supporting the AXIA deep dive investment thesis and DCF valuation assumptions.")

With R$1.2B going to transmission (the largest line item) and a big chunk spent on the Itaipu HVDC modernization. Axia notes it’s fully reimbursed by Itaipu (so it’s capex activity without the same economic burden you’d fear in a normal project)

And it’s not just “maintenance.” Axia is actively adding to its transmission backlog.

In Transmission Auction 04/2025, Axia won lots with RAP of R$138.74M and ANEEL projected capex of R$1.63B, which the company highlights as proof of competitiveness.

transmission auction 04/2025 slide showing ANEEL projected capex of R$1.63B and RAP of R$139M, part of a larger R$17.4B transmission capex pipeline supporting the AXIA deep dive investment thesis and DCF valuation.")

They aggregate the recent auction wins + reinforcements into a total transmission capex opportunity of R$17.4B tied to roughly R$2.4B of associated RAP. They also disclose that the transmission expansion pipeline carries R$1.7B of additional associated RAP between 2025–2030.

The multiple can re-rate as the story de-risks

Even after the rebrand, the market still values Axia like it has one foot in its old life.

Today, the stock trades at 6.9x forward EV/EBITDA. That is on the high end of South American electric utilities.

valuation chart comparing forward EV/EBITDA multiples versus Latin American utility peers including Pampa Energia (PAM), Enel Chile (ENIC), CEMIG (CIG) and EDN, used in the AXIA stock deep dive investment thesis and valuation analysis.")

And the highest Brazilian utility based on TTM EBITDA.

EV/EBITDA valuation chart versus Brazilian utility peers including CEMIG (CIG), Engie Brasil (EGIEY), Equatorial (EQUY), Neoenergia (NRGIY), Light (LGSXY) and SABESP (SBS), supporting the AXIA deep dive investment thesis and rerating valuation case.")

But it is within the range based on forward EBITDA.

EV/EBITDA forward valuation chart versus Brazil utility peers like Engie Brasil (EGIEY), CEMIG (CIG), SABESP (SBS), COPEL (ELPC) and EDN, supporting the AXIA stock deep dive investment thesis and rerating upside case.")

But compared to international utilities, there is a significant gap.

forward EV/EBITDA valuation chart versus North American utility peers including AEP, Entergy, FirstEnergy, Eversource, Southern Co, Duke Energy and Fortis, supporting the AXIA stock deep dive investment thesis and rerating upside.")

I think as a quality utility with growth, the shares should rerate. A move to 11.5x EV/EBITDA is reasonable if two things happen:

Political risk keeps fading into the background.

Axia keeps executing like a real business rather than a government extension.

The March 2025 settlement helped a lot here. It capped state voting power at 10% and removed a huge legacy headache tied to mandatory nuclear spending. That reduces the “Brazil state risk discount” investors apply by default.

Then there’s the business mix.

Axia now looks more like a renewable-heavy platform than a legacy utility. It even reached a 100% renewable portfolio after selling its last thermal asset in 2025. That matters for fund flows. ESG money is not my religion, but it is real demand.

The free cash flow cross-check

I also like to sanity-check valuation with free cash flow.

I forecast Axia to generate R$15B of annual free cash flow by 2027–2028. That supports meaningful shareholder returns. At $13.40, the stock would still trade at a 5% FCF yield which is reasonable for a utility.

At $9.50, AXIA is trading close to the lower bound of P/FCF with a FCF yield of 11%. So yield compression to 5% is realistic based on comparable utilities.

price to free cash flow (P/FCF) valuation chart versus global utility peers including Enel Chile (ENIC), Cemig (CIG), Engie Brasil (EGIEY), Neoenergia (NRGIY) and NRG, supporting the AXIA stock deep dive investment thesis and valuation upside.")

Key Risks: Politics, Power Prices, and Execution

Risk #1. Regulatory/Political Risk

While the worst fears of renationalization have abated, Axia’s past and partial government ownership mean politics is never far away. The Brazilian government (with 32% economic stake) could influence decisions or pursue policies that affect power companies.

For example, there’s always a chance of political pressure to keep electricity prices in check during an election year, or to impose special taxes. The current administration initially opposed the privatization and could, in a extreme scenario, try to meddle if they felt the public is unhappy about tariffs.

The Supreme Court deal limits direct interference, but future governments could try to change laws. Also, the government’s golden share gives it veto power over certain strategic issues, for instance, Axia likely can’t sell nuclear assets or transfer control without approval.

The comforting factor is that Brazil, having gone through the privatization and legal battles, is unlikely to fully reverse course now (that would devastate investor confidence). But it’s a risk that the state could slow down Axia’s full autonomy or load it with some “national interest” projects that aren’t purely profit-driven.

Risk #2. Power Prices, Demand, and Hydrology

Axia’s upside comes from one simple thing: It has more uncontracted energy than most peers.

That also creates risk.

If Brazil’s power market flips into surplus, prices drop. Axia then has to sell more power at weaker rates, and the upside I’m underwriting fades. Brazil keeps adding solar and wind, and in a few years supply could catch up. A slow economy can also soften demand for a while.

Hydrology makes this even trickier.

A wet year usually pushes spot prices down. Hydro output rises, but pricing gets ugly because everybody has water at the same time. A dry year can do the opposite. Prices spike, but generation falls. In extreme cases, the system can even trigger emergency measures like rationing, which adds political risk on top of the commercial risk.

In Q3 2025, Axia lived it. GSF fell from 79% to 65%, meaning hydrology came in well below normal.

showing 3Q25 spot power prices in R$/MWh and GSF percentage, used in the Axia Energia (AXIA) stock deep dive investment thesis to highlight higher merchant pricing upside from uncontracted capacity.")

At the same time, spot prices jumped from roughly R$170/MWh to about R$252/MWh. Lower generation hurt volumes, but higher spot prices helped offset the damage through realized pricing on the energy Axia could sell.

So the impact is mixed.

That’s why Axia needs strong commercial management. Hedging matters. Contracting discipline matters. This is not a “set it and forget it” utility.

As quotas roll off, Axia sells a bigger share of its output at market prices. That raises margin per MWh over time. So even if weather and prices stay noisy, the earnings floor improves versus the quota world.

Hydro is not risk-free. But Axia is moving into a setup where volatility matters less, because each MWh is worth more.

Risk #3. Macro and Currency Risk

Axia operates in Brazil, so I have to respect currency risk. If the Brazilian real weakens, Axia’s ADR can drop even if the company executes perfectly in local currency. The real moves with commodities, politics, and rate differentials.

Brazil’s macro backdrop is also not gentle.

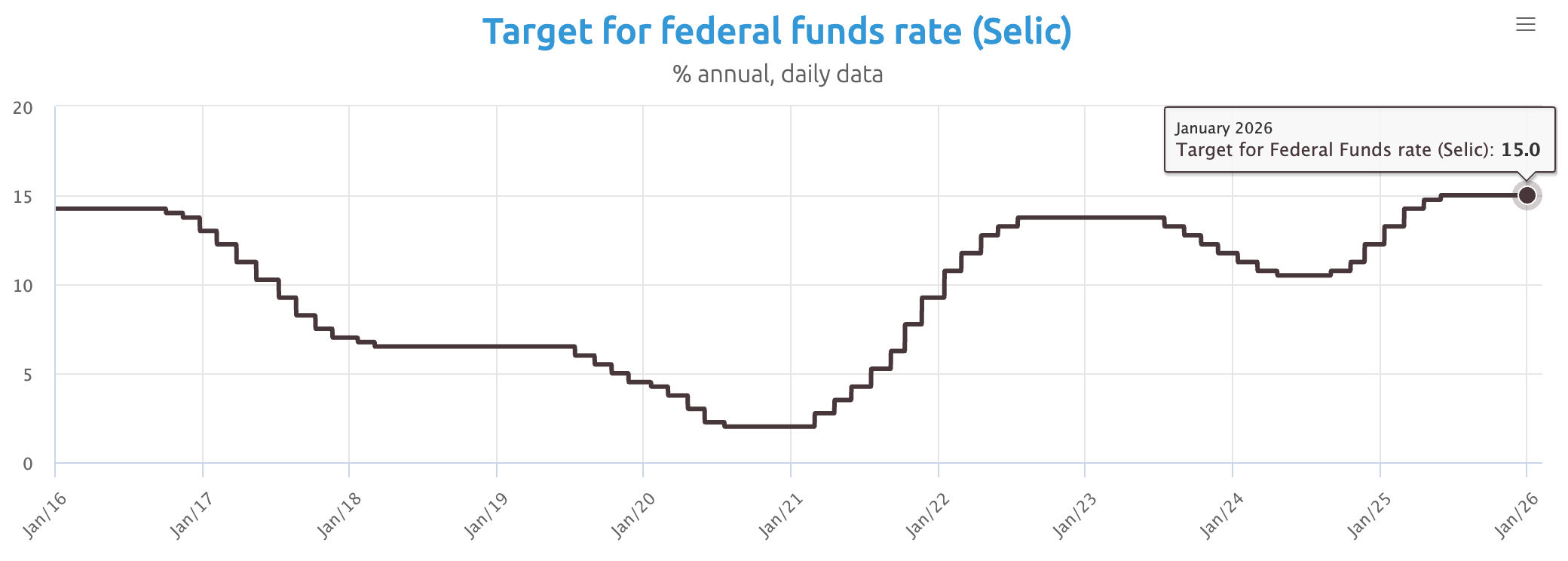

Interest rates are still high. The Selic rate is back around 15% as of January 2026 (after a short period where it looked like rates were heading lower).

That matters because high rates do two things:

They increase the cost of capital, which pressures valuation multiples.

They keep the currency fragile, since investors demand a premium to hold Brazilian risk.

For Axia, the silver lining is that most of its debt is long-dated, so I don’t see a near-term refinancing cliff. But I also can’t pretend rates don’t matter. A meaningful portion of Axia’s debt is indexed to CDI (and CDI+) and IPCA, so higher Selic feeds into higher cash interest expense.

That does not break the story because Axia still generates strong cash flow. But high rates can compress equity sentiment, keep valuation multiples low, and delay the re-rating I’m underwriting.

So even if the thesis plays out operationally, the stock can stay “cheap” longer than it should.

That’s the trade-off with Brazil. You get mispricing and you also get volatility.

Risk #4. Execution Risk

Axia’s story hinges on management executing well. If they misjudge and, say, don’t contract enough and end up with unsold energy, or conversely contract too cheaply and miss out on upside, that could hurt earnings.

Also, implementing the new dividend strategy with share issuance needs to be handled carefully to maintain investor trust (if it’s too confusing or if the preferred shares trade at a discount for some reason, that could backfire).

Integrating new projects (like the data center ventures) is also not a guaranteed success as Axia is stepping a bit outside its traditional role to dabble in hosting data centers, which is cool but new territory (they’ll likely partner with tech firms for that).

And finally, there’s complexity risk. Axia operates through a large web of subsidiaries and consortium structures. Many units are fully owned, but some are not. For example, Axia owns 98% of some entities, 83.71% of Eletropar, 90% of Vale do São Bartolomeu, and it also participates in joint operations like a consortium where it holds 49%. That means results can sometimes include minority interests, partner decisions, and governance friction that investors don’t see in a simple one-line model.

transmission and generation assets in Brazil with concession/contract durations, supporting the AXIA stock deep dive investment thesis on regulated utility cash flows and long-term earnings visibility.")

Aligning all interests and streamlining operations across subsidiaries is a management challenge, though one they’re aware of (they’ve talked about unifying structures for efficiency).

Verdict: Riding the Wave with Axia

I’ll be honest, I love a good comeback story (have you seen Rocky?), and Axia Energia fits the bill.

deep dive investment thesis to highlight volatility, fear-driven selling, and the upside potential in a LatAm utility stock.")

Axia checks all the boxes: a unique catalyst (privatization) that many investors haven’t fully appreciated, a clear fundamental edge (tons of uncontracted capacity in a tightening market), solid management actions (cost cuts and shareholder-friendly moves), and a valuation that still seems too low for what you’re getting. I’m strapping my surfboard to this tide.

União Federal, BNDES/BNDESPAR, FND, FGHAB, Banco do Nordeste, BB Asset, Caixa Asset, Petros and Previ